How AI Compares MLB Odds to Probability: A Pro Analyst’s Guide to Spotting Value

Moneyline odds hide more than they reveal. As a sports analyst who builds AI models for MLB, I will show you how to turn American and decimal prices into clean probabilities, strip the vig, and spot edges. We will fold in real baseball signals like Statcast contact, bullpen fatigue, and weather to translate them into calibrated win chances and smarter bets. Understanding the underlying math is critical because, at its core, this is

how ai predicts baseball scoring

by identifying the true run expectations for each side.

Foundational translation: how AI turns MLB odds into true probabilities

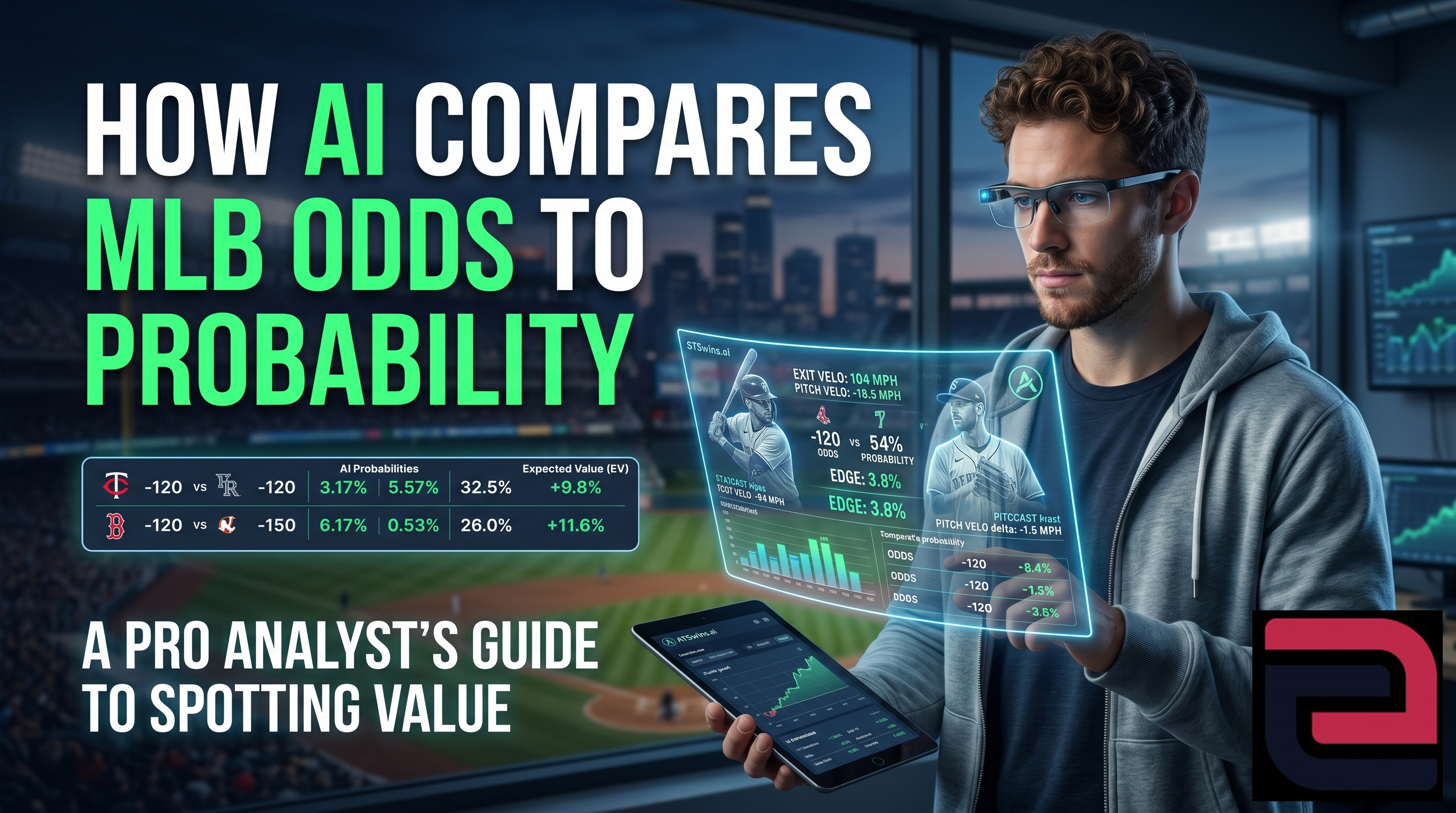

We did not find one definitive source that lays out the AI way to map MLB moneylines to true win probabilities, so we rely on standard market math and public baseball data. That is fine because the translation from odds to probability is mechanical, and the rest is about better inputs and cleaner evaluation. You start with the posted line, which comes in two common formats. For American odds, positive odds involve the formula 100 divided by the sum of X and 100, while negative odds use X divided by the sum of X and 100. If you are dealing with decimal odds, the implied probability is simply 1 divided by the decimal. These are book implied probabilities and they include the sportsbook margin, which is known as the vig. To compare your AI model fairly to the market, you must remove this bias.

For a two-outcome market, which is typical for an MLB moneyline, you compute the raw implied probabilities for both teams using the formulas above. Once you have those, you sum them together and divide each individual raw probability by that sum. That gives you a fair probability where the total equals 1.00. For multi-outcome markets, such as futures or certain three-way lines, the process is the same: you compute the raw probability for every outcome, sum them all, and divide each individual probability by that total sum. This renormalization effectively clears the house margin out of the equation.

Let us walk through a quick example using a standard two-way MLB moneyline where Team A is -120 and Team B is +110. The raw implied probability for Team A is 0.5455, while Team B is 0.4762. When you sum those, you get 1.0217, with that extra 0.0217 representing the vig. If you divide each of those by 1.0217, you get fair probabilities of 0.5340 for Team A and 0.4660 for Team B. You can then convert these back to fair decimals or fair American odds to see the true market price without the bookmaker's cut. When our AI model outputs a win probability that is higher than the no vig market probability for the same team, that difference is where edge can live. A line can be technically correct regarding the margin and liquidity but still be mispriced relative to the true win probability. This happens because models might underweight new information like weather shifts or late lineup news, or the market might be slow to adjust to bullpen fatigue. If your model forecast differs from the no vig market probability, you have identified a signal. You can quantify this by using the posted price to compute the expected value of your bet while using the no vig market probability as a benchmark to ensure your number is not simply an outlier.

Data signals that actually move MLB win probability

Odds translation is the easy part, but getting to the right probability is the real challenge. At ATSwins, our models prioritize specific inputs built for fast ingestion and rigorous auditing. We focus heavily on Statcast contact quality, which includes metrics like average exit velocity, hard hit rate, barrel rate, and expected wOBA. Consistent contact quality predicts run scoring much better than surface stats do, especially in the early parts of the season. We also prioritize pitcher stuff and fatigue. We look at pitch velocity deltas compared to season averages, spin rate changes, and movement profiles. If a starter shows a velocity drop and a tighter gap between their fastball and slider, they might slip a tier in run prevention, which can shift moneyline probabilities by several points. That is a massive difference in the long run.

Platoon splits are also critical, specifically how batters handle different handedness and how lineups manage specific pitch types like high velocity four seamers versus sweepers. A righty heavy lineup facing a righty with a dominant changeup can quietly suppress expected runs. We also track bullpen leverage and the actual pecking order. You have to know who the manager trusts, who is rested, and who is available in high leverage spots. If a team has their top two relievers unavailable, your model should definitely drift the underdog closer. We pay attention to lineup changes, including late scratches and catcher framing swaps, because replacing a framing negative catcher with a top tier framer can improve called strike probabilities and reduce walks. Weather and park effects are non negotiable. Wind direction, temperature, and specific park factors like dimensions and foul ground play a huge role in the run environment. We even look at travel and rest, such as back to back night games across time zones, and umpire tendencies regarding their specific strike zone shapes. Our system ensures that data intake is fresh, auditable, and consistent so that every prediction is based on the most accurate version of the truth. ATSwins aggregates these feeds to generate same day edges and we encourage everyone who builds their own stack to do the same with clear feature versioning.

Modeling and calibration

We treat game winners as a binary classification problem where the target is a home team win. We use supervised learners like logistic regression for a strong, interpretable baseline and gradient boosted trees like XGBoost or LightGBM to handle the complex nonlinearities and feature interactions inherent in baseball data. We often use ensembles to blend these models for better stability. You should always use feature groups like starter metrics, bullpen status, offense against handedness, park factors, and umpire data. Rolling windows, such as 7, 14, or 30 day summaries, are essential because you want to regress to long term means when the sample size for a specific player is small. When refining these inputs, an advanced AI MLB run projection model can also help normalize the expected output against historical league trends to ensure your win probabilities remain tethered to reality.

Calibration is not optional. Raw scores from tree models are often not perfectly calibrated, so you must fix them. We use Platt scaling when the data is modest and a monotonic shift is expected, or isotonic regression when we have higher volume and more complex irregularities. You should always fit your calibration on a holdout subset or through cross validation rather than the training set. Bayesian shrinkage is another essential tool for dealing with small sample landmines, such as rookie call-ups or relievers with limited innings. By regressing these small sample rates toward league or player historical means, you reduce volatility and keep your log loss steady. When dealing with openers or unknown starters, we model a distribution rather than a point estimate for innings and pitch counts. We simulate expected run prevention across pitching segments and then convert that run differential to a win probability using a calibrated link. We avoid data leakage by timestamping every feature to ensure that we are not using closing line information when predicting at the opening line. Finally, we evaluate our work with scoring rules like log loss and Brier score rather than simple accuracy, as those metrics focus on the quality of the probability itself.

Market comparison and staking

Once you have your calibrated probabilities, you compare them to the market and use bankroll control to make sure your edge scales properly. You compute the expected value using your model probability and the posted decimal odds. If the expected value is greater than zero, you have a candidate for a bet, but you must weigh that stake based on the edge and your own risk tolerance. We often require a minimum expected value, such as 1 percent for moneylines, and a minimum probability difference to ensure we are not betting on noise. Market context is vital here, as we might go lighter on signals generated in the early morning and save our higher conviction bets for the period after lineup news is confirmed. When you decide to branch out from just moneylines, these same calibrated inputs can power AI baseball over-under predictions to find value in the total runs market.

We also track line drift from open to close to compute the closing line value, which is a great indicator of how much value you captured. Kelly and fractional Kelly are our go-to methods for bankroll control. We recommend using a fraction of the Kelly criterion, such as 25 or 50 percent, to reduce the chance of massive drawdowns while still allowing for profitable scaling. This is a disciplined approach that respects model risk and market liquidity. We continuously monitor our reliability diagrams to group predictions into bins and check if the realized win rate matches our predicted probabilities. If a 54 percent bin is only winning 50 percent of the time, we know we are overconfident and need to recalibrate our features or our scaling method. As limits increase, the market becomes sharper, and edges often compress. We track the edge half-life by measuring how the expected value changes as we get closer to the first pitch to understand which windows offer us the best consistency. ATSwins tracks these model probabilities alongside posted prices to help you see exactly when the line shifts in a way that impacts the expected value.

Ongoing ops and risk controls

A full baseball season is a grind, and your model workflow must be resilient enough to handle late data, game delays, and rapid roster changes. We automate our scrapes and API pulls to ensure we get lines every few minutes and weather updates hourly. We timestamp every single row of data as of the time it was captured and we never overwrite our raw data tables. We use strict versioning for both our features and our models so that we can ship canary models into production to test their performance before we ever let them influence a real bet.

We have specific alerts for data lags and anomalies. If a lineup does not appear within 30 minutes of the game, our system triggers an alert and automatically downgrades our bet sizing. If we see missing velocity data for a starter, we switch to historical priors to avoid making decisions on bad information. We also stress test our system for doubleheaders, where pitcher swaps happen fast, and for weather delays, where we have to recalibrate availability if a game is resumed. We keep a ledger of every bet we make, including the price at the time of the bet, the model probability, the expected value, and the sources of key features. We then perform a weekly review to determine which features swung the expected value the most and where our model might be overestimating or underestimating based on specific park or umpire variables. This constant auditing loop is what keeps a model profitable from April through October.

Step-by-step: from line screen to bet ticket

The process from line screen to bet ticket is a disciplined sequence. First, you pull the latest moneyline for both teams and record the exact timestamp. Second, you convert those odds to raw implied probabilities. Third, you remove the vig using the division method we discussed earlier. Fourth, you generate your model probability for the exact bet scope, ensuring you use only the features available at that timestamp to prevent leakage. Fifth, you compute the expected value at the posted price. If the expected value is not positive, you pass on the bet entirely. Sixth, you check your market relative threshold to ensure the gap between your probability and the no vig market probability is wide enough to justify the risk. Seventh, you size the bet using your chosen fraction of the Kelly criterion, taking into account any necessary caps based on your bankroll. Eighth, you log the bet, including all inputs and the reasoning behind the stake. Ninth, after the game concludes, you update the results and track metrics like closing line value and realized profit. Tenth, you perform a weekly review to look at your calibration metrics, determine where your model struggled, and make the necessary adjustments to your shrinkage or feature weights for the following week.

A short checklist for MLB model inputs

When building your inputs, check the starting pitcher for velocity deltas and command trends. Make sure you check the bullpen for the availability of your top three relievers and consider handedness coverage for late innings. For the offense, look at rolling metrics against the starting pitcher's handedness and analyze how they handle specific pitch types. Do not forget defense, particularly the defensive runs saved or outs above average at specific positions and the impact of the catcher. The context is everything, so always factor in park effects, the day's weather, including the wind vector, and the umpire's historical strike zone tendencies. Finally, look at the market to compare the opening price to the current price so you can gauge the recent drift and calculate an accurate no-vig market probability.

Calibration, reliability, and humility

Even the best models in the world fall victim to overfitting. You must watch out for early-season illusions where hot or cold starts do not reflect underlying contact quality changes. You must watch out for small sample bullpen results that fluctuate wildly. You must also be wary of the volatility of daily lineup strength and the potential for unmodeled injuries or illnesses. Use reliability diagrams to force yourself to be accountable. If you assume your 58 percent bin is going to win at a certain rate and it keeps missing that target, all your staking math is fundamentally flawed. You must have the humility to recalibrate using isotonic methods or to reweigh features that are pushing your probabilities into unrealistic territory. Tracking your log loss and Brier score over rolling periods is the only way to ensure your model stays sharp. If you consistently fail to beat the closing line, you need to reassess your information edge. A smaller, well-calibrated, and highly selective model will almost always outperform a large, noisy model that forces too many bets on the board.

How ATSwins fits into your process

ATSwins uses the exact math we have laid out here combined with fast, auditable data. We deliver data-driven picks and probabilities for MLB sides, totals, and player props. We provide betting splits as context, which can be helpful for timing your entries even if they are not predictive on their own. We offer robust bankroll and profit tracking so you can monitor your expected value against your realized performance. Our system monitors calibration behind the scenes, so our reliability checks inform you when you should dial back your aggression. If you prefer to screen lines yourself, our platform allows you to see model probabilities next to live prices in one central hub during the important afternoon lineup window. We turn complex data into actionable insights so you can focus on the betting, not the busy work.

Frequently Asked Questions (FAQs)

What does “how AI compares MLB odds to probability - find value” mean in simple terms?

It means we turn sportsbook MLB odds into win probabilities, then stack those against an AI model’s true game probabilities to see where the price is off. If my model says a team wins 54 percent and the no vig market says 49 percent, that gap is value. You are not guessing; you are comparing two numbers and betting only when your edge is real and measurable.

How do I convert MLB moneyline odds so AI can compare odds to probability and find value?

Step one is to convert American odds to implied probability. Negative odds like -130 result in a probability of 130 divided by 230, which is approximately 56.5 percent. Positive odds like +150 result in 100 divided by 250, which is 40 percent. Step two is to remove the vig. For a two team market, add both implied probabilities and divide each side by that total. If the sum is 102.5 percent, your fair probabilities are 56.5 divided by 102.5 and 46.0 divided by 102.5. Step three is to compare your model probability to that no vig probability. If your model is higher for the favorite, you have found value. You can pull daily contact metrics from Baseball Savant to drive these inputs.

Which data helps most when AI compares MLB odds to probability to find value?

From my day to day modeling, I find Statcast contact quality like expected wOBA and barrel rate are the most important. Starting pitcher status and bullpen fatigue are also vital, and FanGraphs has excellent bullpen usage tables and pitch logs. Confirmed lineups are massive because late scratches move true win rates much more than people realize. Weather and park factors change the run environment, and umpire tendencies regarding zone size can tilt strikeout and walk rates. Feed those into a calibrated model and only act when the model beats the no vig line by a set threshold.

How does ATSwins.ai support “how AI compares MLB odds to probability - find value” for everyday bettors?

ATSwins.ai is an AI powered sports prediction platform offering data driven picks, player props, betting splits, and profit tracking across the major sports leagues. We provide free and paid plans to give bettors the insights and guides they need to make smarter, more informed decisions. From my analyst lens, the edge is in how ATSwins aggregates signals and presents them with clear confidence levels and tracking. This ensures you can see when the AI probability actually beats the de vigged market price rather than relying on hot takes. It keeps you focused on value and bankroll health.

After AI shows an edge when comparing MLB odds to probability to find value, how should I size the bet?

Keep it simple by using fractional Kelly. Your stake should be your edge divided by the decimal odds, then further reduced by a fraction like 0.5 or 0.25 if you want extra safety. This smooths out your swings while still rewarding you for bigger edges. You should always cap your risk per play, typically between 0.25 percent and 1 percent of your bankroll, to protect yourself. Track your results and your calibration. If you find your 60 percent edges only win 53 percent of the time, dial your stakes down and re tune your model. Note that timing matters, as steam near the lineup lock can erase value, so place bets when your edge clears all fees and slippage.